I work with a number of people, typically high-net-worth individuals with six-figure incomes, to counsel them on retirement savings. What separates those who are successful from those who will have to work until they die? It is not their level of income. Those who successfully save for retirement right size their spending to fit their income.

Here are the three things that make all the difference:

1) Save first.

2) Ignore the neighbors.

3) Pay your bills.

#1: Save first

The most crucial step in the process is to get the money out of reach, before you even miss it. Get at least six to twelve months of expenses into a savings account for a rainy day/emergency fund (only to be used during monsoons, not drizzles). Then, once achieved, direct money from your paycheck right into the 401k or (and!) to a savings account that you consider out of reach. It is old-fashioned, yes, but it works! You should always contribute the maximum that the government will allow to tax-favored accounts, and then more to another account. For 2019, the maximum 401(k) contribution amount is $19,000 for those under 50 years old and $25,000 for us older folks

#2: Ignore the neighbors

Watch what all of your friends do, and do the opposite! Frankly, keeping up with the neighbors usually drives folks into financial ruin. Maybe you even need to change neighborhoods. The largest expenditure for most folks is housing – and in America we often have too much house. This is the biggest structural change you can make to benefit your financial future, as Americans spend 30% or more of their incomes on housing, and often the housing is just too big for the family it houses.

Okay, this is typically the part of the story where you expect to be berated about drinking $4 coffee from Starbucks when it costs just cents on the dollar to make it at home (check that box). I’m not going to do that. Here’s what I recommend instead. You must start tracking your own spending (Mint is a great online free tool that makes it very convenient to do this), and then, once you have the facts, prioritize your spending yourself. I cannot preach to you about your priorities because they are uniquely yours. If you want to spend money on health clubs or Peloton® when you can get plenty of exercise for free at home using just your body weight and free online apps if you require “personal training” (or my favorite, running), new cars every three years (whereas used cars are much more economical), paying bills late and incurring late fees, private schools and out-of-state colleges (when the local school offers the same curriculum at a much lower cost), eating out, and subscribing to services that you don’t even remember – that’s your choice. At least if you track the costs, you will be aware of these decisions and make conscious ones.

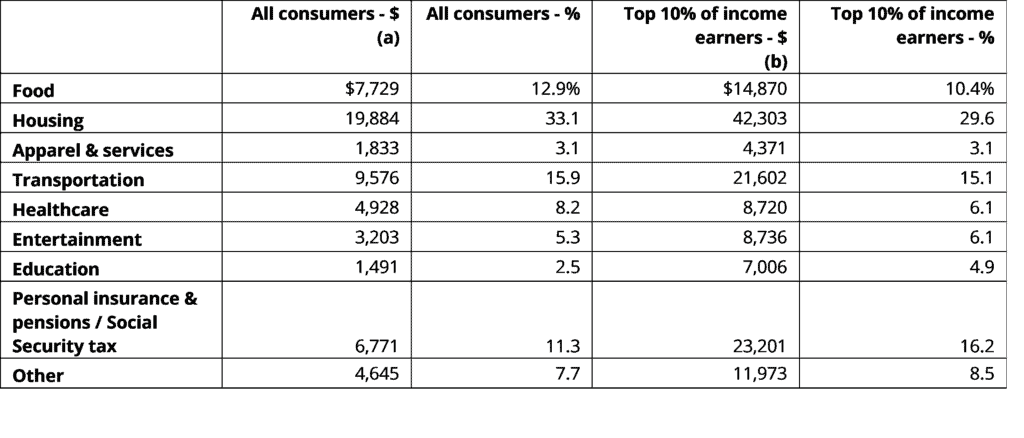

By the way, here are the averages of what people in America spend their money on (excluding taxes) based on the government’s 2017 Consumer Expenditure Survey:

(a) Mean income before taxes = $73,573

(a) Mean income before taxes = $73,573

(b) Mean income before taxes = $247,174

#3: Pay your bills

You must avoid consumer debt, the associated interest and late fees like the plague. This means no consumer debt. Pay off your credit cards each month, on time. Do not borrow to buy automobiles. If you cannot afford to save and pay cash for the car, buy something more affordable. If you need money for a true emergency, you have an emergency fund. If you cannot pay for an item in cash, this is one indicator that it is too expensive for you. Okay, yes, you can borrow to buy your house, but you should only take out a 15-year loan which can be paid off before the kids go to college. Some say your home is your biggest investment – it is not. Your home is your residence, and you have got to live somewhere, so don’t consider it an investment unless you plan to sell it and downsize – or be homeless!

The bottom line

The takeaway here is that every person is different. You should enjoy your money – you work hard for it. However, your decision making should be conscious and in advance, realizing that every expenditure is a trade-off for alternative spending and future spending in retirement. Be smart!

Shawn W. Hardister CPA, CFP®, regularly assists closely-held companies and their owners realize financial success. He is a tax and financial planning partner who specializes in professional services firms, particularly law firms and physician practices.

Shawn W. Hardister CPA, CFP®, regularly assists closely-held companies and their owners realize financial success. He is a tax and financial planning partner who specializes in professional services firms, particularly law firms and physician practices.

0 Comments